Licensee Liability Rating – A Complete Guide

Introduction

When you operate a licensed business—whether in construction, healthcare, finance, or other regulated sectors—your licensee liability rating plays a critical role in shaping your future. Much like a credit score for professional responsibility, it affects your insurance premiums, eligibility for contracts, regulatory standing, and even your ability to form partnerships.

Despite its importance, many business owners remain unaware of how these ratings work or how much they influence long-term success. This guide explains what a licensee liability rating is, why it matters, how it’s determined, and what you can do to improve yours.

What Is a Licensee Liability Rating?

A licensee liability rating is an evaluation of the potential risk a licensed professional or business poses to clients, customers, and the public. Insurance companies, regulators, and potential business partners rely on this rating to determine how trustworthy, compliant, and safe your operations are.

Think of it as a risk scorecard. Unlike a financial credit score, which focuses on borrowing and repayment behavior, liability ratings assess your professional conduct, claims history, industry practices, and risk management protocols.

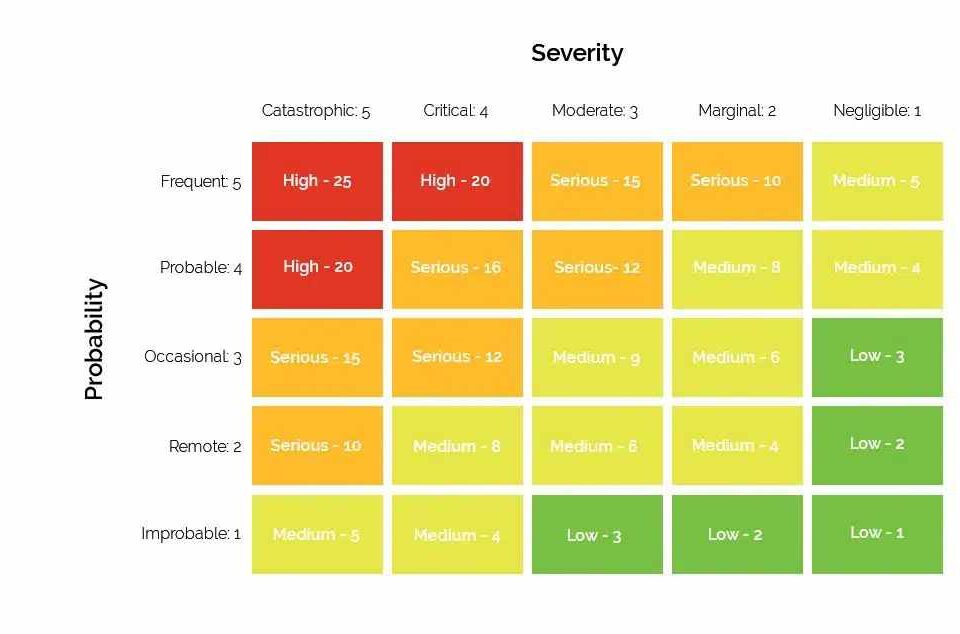

Common factors considered include:

- Claims history – lawsuits, settlements, or payouts

- Industry type – some sectors are naturally riskier

- Business size – larger operations often face greater exposure

- Safety protocols – risk prevention systems and training

- Financial stability – ability to cover potential liabilities

Why Your Liability Rating Matters

Your licensee liability rating impacts nearly every aspect of your business operations.

1. Insurance Premiums

Insurers use ratings as their main tool to set premiums. A strong rating lowers your costs significantly, while a poor one can make coverage unaffordable—or even unattainable.

2. Contract Opportunities

Government agencies and corporations often require a minimum liability rating to qualify for bids. If your rating doesn’t meet the threshold, you’re disqualified before you even submit a proposal.

3. Regulatory Compliance

While liability ratings don’t usually trigger regulatory penalties on their own, they provide context to licensing boards during reviews, renewals, or investigations.

4. Business Partnerships

Franchisors, investors, and joint venture partners want to avoid unnecessary risks. A poor rating signals potential trouble, limiting partnership opportunities.

5. Access to Capital

Banks and investors increasingly evaluate liability ratings as part of their decision-making. Businesses with poor ratings are often viewed as high-risk investments.

Key Factors That Influence Your Rating

Claims History

- Number of claims filed

- Severity of damages or settlements

- Frequency of incidents

- Time since last claim

Even claims without payouts may reduce your score if they reveal patterns of poor practices.

Industry Risk Profile

Different industries carry baseline risks. For example, healthcare and construction are higher-risk than accounting or consulting.

Financial Stability

Stable businesses are less likely to collapse under liability claims. Agencies look at revenue consistency, profit margins, cash flow, and insurance coverage levels.

Risk Management Practices

Demonstrated policies, employee training, safety protocols, and documentation can significantly improve your rating.

Regulatory Record

Past violations, suspensions, or disciplinary actions weigh heavily on your rating. Compliance and continuous education can strengthen your profile.

Table 1: Core Elements of Licensee Liability Rating

| Factor | Description | Impact on Rating |

| Claims History | Past lawsuits, settlements, and payouts | High |

| Industry Profile | Inherent risk level of your sector | Medium |

| Financial Stability | Revenue, margins, and insurance coverage | High |

| Risk Management | Safety policies, training, and documentation | High |

| Regulatory Compliance | Licensing and certification records | Medium |

How to Improve Your Licensee Liability Rating

1. Implement Risk Management Systems

- Create clear protocols for high-risk activities

- Train employees regularly and document participation

- Use quality control checks and audits

- Keep thorough communication records with clients

2. Invest in Training & Education

- Update staff on industry regulations

- Provide customer service training to reduce disputes

- Document every training activity for rating reviews

3. Maintain Comprehensive Documentation

- Record client communications, agreements, and outcomes

- Track incidents and corrective actions

- Store compliance certifications and licenses

4. Strengthen Financial Stability

- Maintain adequate insurance coverage

- Manage debt responsibly

- Improve cash flow consistency

5. Review Insurance Regularly

Work with insurers to ensure your policy limits match your current exposure levels.

Table 2: Practical Steps to Boost Your Rating

| Action Plan | Benefit | Documentation Needed |

| Regular employee training | Fewer mistakes, reduced claims | Certificates, attendance logs |

| Quality control audits | Identifies risks early | Audit reports |

| Client communication logs | Reduces disputes | Emails, summaries |

| Insurance policy updates | Adequate coverage | Policy documents |

| Compliance tracking | Stronger regulatory record | Certificates, renewals |

Common Myths About Licensee Liability Ratings

- Myth 1: “A clean record guarantees a great rating.”

Reality: Other factors like financial health and risk management also matter. - Myth 2: “Small businesses don’t need to worry.”

Reality: Even small businesses are scrutinized and often face proportionally greater risk exposure. - Myth 3: “Ratings only matter for insurance.”

Reality: Ratings influence contracts, partnerships, and financing too. - Myth 4: “You can’t improve a bad rating quickly.”

Reality: With strong improvements, results can be seen within 12–18 months.

Conclusion

Your licensee liability rating is more than just a number—it’s a powerful business asset that influences costs, contracts, and credibility. By taking proactive steps in risk management, financial planning, documentation, and compliance, you can significantly improve your rating and strengthen your long-term position.

Improvement isn’t a one-time effort. Regular reviews, continuous training, and transparent practices ensure that your rating remains strong—unlocking better insurance rates, more contracts, and sustainable growth.